The Agentic Finance Stack Protocols Part 1: Payment Rails

Every AI agent that buys, sells, or pays needs to move money. But modern payment systems were built for humans, not autonomous code. Let’s explore how money actually moves today—and why it matters for agentic commerce.

In this post, we’ll explore the first layer of the Agentic Finance Stack: the foundational payment protocols and rails that move money in today’s financial system.

There are many layers of protocols, networks, and systems that enable modern payments. We won’t cover all of them here. Instead, we’ll focus on the key technologies that teams building agentic systems need to understand.

Any payment between AI agents, or between agents and other systems (like MCP servers), must move across a payment rail. While we expect stablecoins to become the primary payment instrument for agentic systems, they won’t be the only ones. Understanding how traditional rails work—and how they differ from stablecoin systems—will help AI builders design reliable, compliant, and interoperable agentic payments.

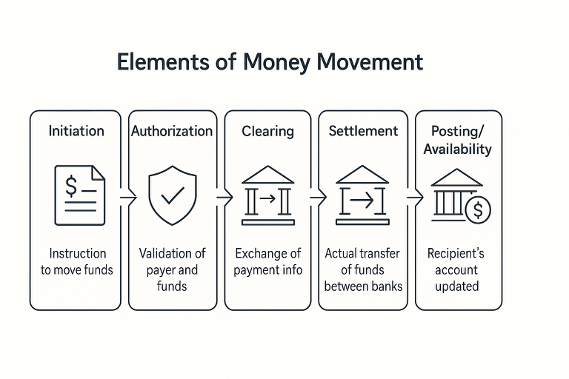

Key Payment Concepts

Most traditional (non-stablecoin) payment systems share five foundational steps in the flow.

Figure generated by ChatGPT 5 Auto.

These steps may not always occur in strict order. For example, clearing and posting may happen before settlement. Among these, settlement is often the most critical step—this is when funds are finally transferred between financial institutions to discharge obligations.

Another essential concept is liquidity—the availability of funds in the right form and location at the moment they’re needed to settle a transaction. If liquidity is unavailable, even valid payment instructions can’t be completed. Liquidity management is central to payment operations and will be revisited in later posts.

Bank-to-Bank Payments

Payments between banks form the backbone of the global financial system. Many of the systems still in use today were established decades ago, but remain critical underpinnings of modern money movement.

While our long-term goal is to replace legacy rails with stablecoin-based systems and new protocols designed for AI agents, these older systems will remain relevant for years to come.

Wires

Wire transfers date back to the 19th century, when banks used telegraph messages and physical couriers to move funds. Today, modernized systems like Fedwire (U.S.) and SWIFT (international) enable secure, high-value transfers.

-

Fedwire settles transactions between banks’ accounts at the Federal Reserve, enabling fast and final settlement compared to most other traditional rails.

-

Wires are relatively fast, support large-value transactions, and offer finality (they can’t be reversed by the sender).

-

However, they’re bank-to-bank only, operate on limited hours, carry high per-transaction costs, and include minimal message data.

While agents could technically initiate wire transfers, they are ill-suited for real-time, high-frequency, or low-value use cases that agentic systems typically need.

ACH (Automated Clearing House)

The ACH network, launched in the 1970s as an electronic alternative to paper checks, is the most widely used U.S. payment system. In 2024, ACH processed over 31 billion transactions, moving more than $80 trillion.

-

ACH transactions are batched and settled several times per day through the Federal Reserve.

-

Typical settlement occurs within 1–2 business days, though Same Day ACH now enables faster transfers in many cases.

-

ACH supports both credit (push) and debit (pull) payments, with low costs and broad adoption.

However, ACH is not instant, and transactions can be reversed for a period. These characteristics make it unsuitable for millisecond responsiveness or always-on agentic use cases. It may serve as an underlying layer in hybrid systems, but is unlikely to be the primary interface for AI agents.

Real-Time Payments (RTP)

To modernize bank transfers, new real-time payment systems have emerged—such as The Clearing House RTP and FedNow.

-

These systems operate 24/7, offer instant or near-instant settlement, and are designed for finality (though limited recall mechanisms exist).

-

They support low-cost, irreversible, and account-to-account payments.

-

However, they remain bank-to-bank systems, often capped in transaction size (e.g., $500K), and require integration with bank partners.

RTP systems are a step toward continuous, programmable money movement, but their current design and access constraints make them challenging for autonomous AI agents to use directly.

Consumer and Business Transactions

Above the bank rails sit payment networks and services that enable everyday consumer and business transactions. These systems depend on bank rails under the hood but add their own protocols and features.

Cards

Credit and debit cards are ubiquitous in global payments, connecting billions of consumers and merchants.

While their global reach is unmatched, card networks introduce challenges for agentic systems:

-

Reversibility (chargebacks) undermines transaction finality

-

High fees and multi-day settlement increase costs

-

Cardholder data requirements create security and compliance hurdles for non-human agents

As a result, card networks are poorly suited for autonomous AI transactions.

Peer-to-Peer (P2P) Systems

Platforms like Venmo and Cash App offer instant, low-cost, irreversible transfers within closed networks.

While convenient for human users, their closed-loop nature (you can only pay other users of the same platform) makes them inflexible for agents that need to transact across ecosystems.

Remittance Networks

Cross-border remittance providers such as Western Union and MoneyGram allow near-instant transfers between countries by maintaining liquidity pools in each region.

For example, when sending USD from the U.S. to MXN in Mexico, the provider pays out immediately from local reserves, then periodically rebalances across borders.

This pre-funded model enables speed but at the cost of high fees and closed access. These systems could eventually expose APIs for agentic use, but integration barriers and cost structures remain significant.

Stablecoins

Stablecoins like USDC represent a new class of payment instrument with properties well-aligned to agentic commerce:

-

On-chain settlement: Transactions are recorded and finalized on public blockchains, independent of central banks.

-

Instant or near-instant settlement, limited only by blockchain confirmation times

-

Low fees relative to traditional rails

-

Programmability via smart contracts, enabling autonomous, conditional, or recurring payments

-

Irreversibility, ensuring finality once confirmed

-

Fully digital, with machine-native interfaces suitable for AI execution

However, stablecoins also introduce new considerations:

-

Technical integration requires blockchain infrastructure and key management

-

On/off-ramp friction remains, though improving

-

Irreversibility can be a drawback in cases where refundability is desirable

-

Compliance obligations still apply—companies transacting with stablecoins must meet AML/CFT requirements, often requiring licensed partners or custodians

While stablecoins are not yet a complete replacement for traditional rails, they represent the most promising foundation for autonomous, programmable, and global agentic payments.

Additional Considerations for Agentic Systems

To design effective payment systems for AI agents, builders should also consider:

-

Cross-border and FX handling – Many agentic transactions will be global; understanding exchange rates and messaging standards (e.g., ISO 20022) is essential.

-

Security and key management – Agents must safely store and use private keys or API credentials to authorize transactions.

-

Interoperability – Bridging between fiat rails, stablecoins, and Layer 2 networks will be necessary for broad agentic functionality.

-

Regulatory compliance – Even autonomous systems must comply with KYC, AML, and licensing frameworks.

These considerations go well beyond the capabilities and core competencies of most teams building agentic systems, and this is where the next two layers of the agentic commerce stack, infrastructure and banking, come into play. An AI bank will provide a trusted, regulated financial institution with the ability to address these considerations and the technical capabilities to empower teams working at the solution layer in the stack to build quickly and confidently, without having to worry about these layers of the stack

Looking Ahead

In this post, we introduced payment rails as a foundational component of the A-Commerce protocol layer. They determine how money moves and settles—whether between banks, users, or agents.

In Part 2, we’ll explore the agentic protocols that sit atop these rails—enabling agent-to-agent and agent-to-merchant transactions with trust, programmability, and compliance built in.